Insurance for Home Gym: 7 Powerful Reasons You’re at Risk

Insurance for Home Gym are frequently neglected by enthusiasts who spend a lot of money establishing individualized workout areas. While the hassle-free nature of home workouts cannot be denied—providing flexibility, privacy, and long-term financial savings—the monetary repercussions of possible damage or liabilities can be severe. Whether it’s a burst basement that destroys thousands of dollars’ worth of equipment or a visitor getting hurt during an exercise routine, the potential is there. Learning to appreciate the value of covering your home gym is not merely a matter of insuring the equipment—it’s about protecting your investment, your economic security, and your peace of mind.

Home gyms have gained immense popularity over the past few years, especially due to global events like the COVID-19 pandemic that restricted access to commercial fitness clubs. This trend has also prompted homeowners to transform spare rooms, garages, or basement areas into fully equipped exercise areas with high-end equipment, free weights, mirrors, and even virtual training systems. But as the trend increases, so do the hazards. Most homeowners have no idea that their basic insurance policies may not be sufficient to cover this specialized area. From theft and fires to accident liability, the distinct characteristics of home gyms require special care when it comes to insurance planning.

Table of Contents

1. Understanding the Importance of Insurance for Home Gym

Protecting Your Fitness Investment:

Creating a home gym isn’t merely a lifestyle choice—it’s a significant money outlay. Even a minimal home gym installation, reports wod.guru, can range from $1,000 to $5,000, with more sophisticated arrangements involving commercial-quality equipment well over $10,000. Loss of the equipment in the event of a fire, flood, or burglary could be costly. Most standard homeowners’ policies, however, either exclude gym equipment or set stringent caps on payback amounts.

That is where Insurance for Home Gym comes in. Rather than counting on limited coverage that will only pay out for a portion of your loss, having specialized insurance guarantees that expensive items like treadmills, power racks, smart bikes, and lifting platforms are covered in full or replaced promptly.

Tip: Save receipts and serial numbers of everything you have. Notify your insurer when you acquire new or upgrade equipment.

Addressing Liability Risks at Home:

In addition to protecting equipment, liability is a concern for growing businesses—particularly for those who have friends, family members, or even clients coming to use their gym. One accident, like slipping on a mat or straining a back on a lift, could lead to expensive legal proceedings. According to nasm.org, home-based personal trainers and gym owners are most vulnerable to such liability risks.

Home gym space insurance should also have personal liability coverage that covers you if a person gets injured from using your machine. Without it, you can end up shelling out thousands in medical bills or attorney fees.

Liability Preparedness Checklist:

- Install proper flooring and ventilation.

- Display safety signs or instructions.

- Never permit unsupervised visitors to operate equipment.

- Discuss with your insurer how to extend your liability coverage.

2. Evaluating Your Current Home Insurance Policy

Coverage Limitations You Might Not Know About:

Most home owners believe that their current insurance plans automatically cover everything within the home—be it a personal gym. But not always. Westfield Insurance says that your Insurance for Home Gym policy could treat gym equipment as personal property that typically comes with a limitation on the coverage amount. The limit may even be as low as $1,500–$2,000—something lower than most individuals invest in creating a serious fitness room.

In order to get enough protection, you should check whether your policy limits will completely cover the value of your gym if it is stolen, burned, or damaged from water. In case they will not, then it is time to take into account insurance for home gym equipment in the form of a rider, endorsement, or standalone policy.

What to check:

- Check the personal property part of your policy.

- Check for sub-limits on electronics or fitness equipment.

- Inquire with your insurer whether they can raise your coverage.

Exclusions That Could Cost You:

Most insurance products also have exclusions that might expose you to risks. For instance, damage resulting from power surges, mechanical breakdowns, or misuse may not be covered under a typical homeowners’ policy.

Here’s where home gym equipment insurance can become more customized. Including a scheduled personal property endorsement or equipment breakdown coverage can cover these gaps and protect against more specific events—such as a treadmill motor failure or a rowing machine short circuiting from a storm.

Situations usually excluded in standard home insurance:

- Electrical surges ruining smart devices.

- Moisture accumulation in a garage gym leading to rust.

- Incorrect installation causing machine malfunction.

Pro Tip: Think about having a dedicated electrical line for your gym equipment and surge protectors to avoid common problems.

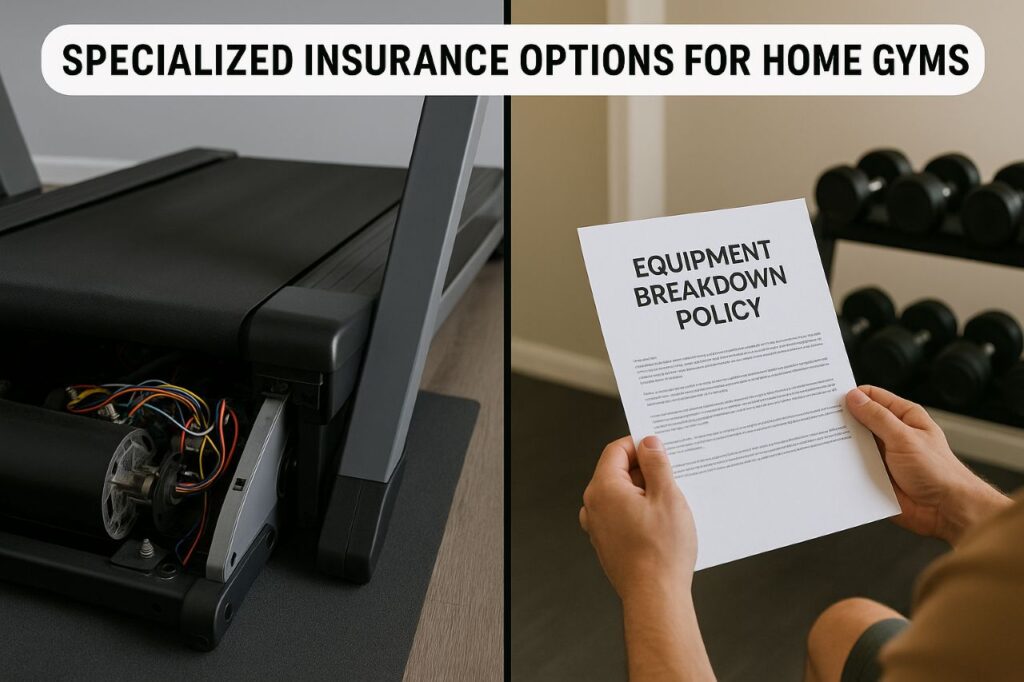

3. Specialized Insurance Options for Home Gyms – Insurance for Home Gym

Equipment Breakdown Coverage:

Most typical homeowners’ policies will not cover damage resulting from mechanical or electrical breakdown of exercise equipment. This can be frustrating when costly equipment like a NordicTrack treadmill or a Peloton bike fails unexpectedly. That’s why equipment breakdown coverage is among the most utilitarian types of insurance for home gym enthusiasts.

As per The Zebra, such an add-on can provide coverage for repairs or replacement in case your fitness equipment breaks down due to internal problems—not merely external catastrophes.

Protected by Equipment Breakdown Coverage:

- Treadmill motor malfunctions.

- Elliptical console short circuits.

- Smart fitness screens or mirrors.

- Resistance training systems overheat.

Tip: Combine this coverage with your Insurance for Home Gym policy to pay lower premiums and get additional protection for other appliances, too.

Personal Umbrella Policy: Insurance for Home Gym

If you frequently have friends, guests, or even customers utilizing your home gym, a personal umbrella policy (PUP) can be an insurance safety net. A PUP adds on to your liability coverage in excess of what your homeowners’ policy covers. So, if a gym injury results in someone suing you, you’re not out tens of thousands of dollars.

For example, if your homeowners’ policy offers $300,000 in liability coverage, but you’re sued for $1 million, a PUP can cover the remaining $700,000.

When to consider a personal umbrella policy:

- You host fitness classes or group workouts.

- You rent your gym space occasionally.

- You have high-net-worth assets to protect.

Insight from III.org: “An umbrella policy is an inexpensive way to add an extra layer of liability protection.”

Why it matters: Personal injury suits can be costly. Insurance for Home Gym should have umbrella coverage if you anticipate any third-party use.

4. Business Use Considerations – Insurance for Home Gym

Running a Personal Training Business from Home:

If your home gym is being used for business purposes—such as providing personal training sessions or fitness coaching—it dramatically shifts your insurance requirements. Most homeowner’s insurance policies squarely exclude business activity. That is to say, any personal injury, damage to property, or loss during business hours may not be covered.

This is where Insurance for Home Gym setups with business use comes in. You’ll need a home-based business insurance policy or a commercial liability policy designed for personal trainers or fitness instructors. As nasm.org explains, liability insurance is a must-have for fitness professionals—even when working from home.

Key protections you’ll need:

- General liability coverage.

- Professional liability (errors & omissions).

- Equipment damage or loss.

- Client accident and injury coverage.

Tip: Maintain waivers on file for all clients and require them to sign an acknowledgment of risk prior to any workout session.

Hosting Group Classes or Paid Sessions: Insurance for Home Gym

Running bootcamps, yoga sessions, or small-group fitness classes in your home gym? While it can be lucrative, it adds serious liability risks. Imagine someone trips on a kettlebell, tears a ligament, and sues you—your homeowners’ insurance won’t help unless you’ve declared the space for business use and updated your policy.

In this case, the right Insurance for Home Gym setup would involve:

- A Business Owner’s Policy (BOP) – property, liability, and business interruption insurance bundled together.

- Product liability coverage – if you recommend or sell supplements or fitness equipment.

- Commercial umbrella insurance – additional liability coverage.

As Hiscox explains, fitness professionals working from home require specific protection in order not to lose everything.

Checklist if you operate a business out of your gym:

- Revise local zoning or permits.

- Place visible safety instructions.

- Include commercial liability in your current policy.

- Maintain good client and injury logs.

5. Steps to Ensure Adequate Coverage – Insurance for Home Gym

Create a Detailed Home Gym Inventory: Insurance for Home Gym

The initial step towards acquiring the appropriate insurance for home gym equipment is taking inventory. With no clear documentation, you can expect processing delays or lowball payments for claims following loss or damage. Insurers typically request proof of purchase and approximate value when settling claims.

Documenting your gym:

- Document all items from big machines to resistance bands.

- Add brand, model, serial number, and date purchased.

- Save electronic copies of receipts and guarantees.

- Capture clear images or videos displaying the entire gym equipment setup.

Extra Tip: Utilize apps such as Sortly or Encircle to digitally organize your gym stock.

Once your stock is prepared, distribute it to your insurance agent to determine if your existing policy limits need to be modified.

Speak with an Insurance Professional:

Most individuals aren’t familiar with the nuances of insurance language, endorsements, or exclusions. That’s why one of the wisest things to do is have a chat with a licensed agent. Not every agent will automatically suggest Insurance for Home Gym equipment unless you ask—so be clear about your requirements.

Insurance questions to ask your agent:

- Does my existing homeowners policy cover my equipment?

- What are the restrictions on electronics or exercise equipment?

- Do I require extra endorsements for power surge or flooding damage?

- What if a guest is injured while working out?

- Are business activities excluded or covered?

As Insurance Information Institute (III) recommends, business usage and high-value equipment entail special coverage modifications—not merely one-size-fits-all plans.

Tip: Always notify your insurer if you install costly equipment or start offering paid sessions in your gym.

6. Real-Life Scenarios Highlighting the Need for Insurance for Home Gym

Damaged Equipment from Electrical Malfunctions:

Suppose you spent $3,000 on a smart treadmill with screen features. A heavy thunderstorm passes through your region one evening and induces a power surge that destroys your treadmill’s motor and display unit. You call your insurer, who informs you that your basic home insurance won’t cover electrical failures unless you have equipment breakdown coverage.

This is a straightforward situation where having the right Insurance for Home Gym can make or ruin your finances. A policy with extra equipment protection would have covered you for the repair or replacement fees.

Do not make this error:

- Fit a surge protector on all gym electronics.

- Inquire about electrical or mechanical breakdown coverage from your insurer.

- Save digital warranties and purchase receipts as a backup.

Guest Injury During Workout: Insurance for Home Gym

Now consider another scenario: your friend visits and wants to try your new rowing machine. During their session, they fall and twist their ankle badly. They later file a claim for medical costs and lost wages, alleging negligence on your part.

Without personal liability coverage on your Insurance for Home Gym, you might be personally responsible for covering those costs. Depending on the injury and legal process, this could translate to thousands of dollars in payouts—not to mention attorneys’ fees.

How to avoid liability problems:

- Never have guests alone in your gym.

- Provide proper flooring and slip resistance.

- Incorporate signs for safety reminders.

- Check your policy for personal liability coverage.

Flooded Basement Destroys Your Gym:

Suppose your basement home gym is flooded by water when one of the pipes bursts when you are not around, on vacation. Upon your return, your weight bench, treadmill, and rubber floor are destroyed by water damage. You make a claim only to discover that you are not covered for flood damage under your existing homeowners’ policy.

In such a scenario, Insurance for Home Gym would not work unless you have additional flood insurance or water damage endorsements. FEMA states that an inch of water can damage more than $25,000.

Useful Tips:

- Raise electronics and machinery off basement floors.

- Install water sensors around plumbing lines.

- If your home gym is underground, consider flood insurance.

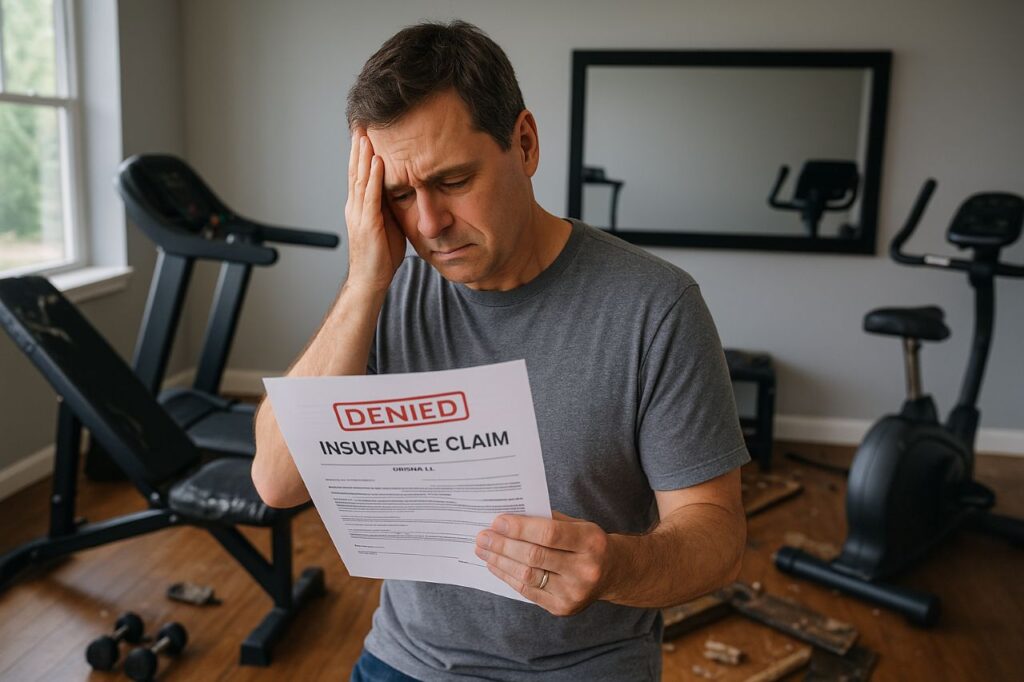

7. The Cost of Skipping Insurance

Why Going Uninsured Is a Financial Risk: Insurance for Home Gym

Forgetting to include home gym coverage in your policy might look like a money-saving hack in the short term—but it can end up costing you significantly more in the long term. Without proper insurance, you’re leaving yourself vulnerable to losses such as equipment loss, injury, and even lawsuits that can deplete your savings or lead to claim denial.

One injury claim alone may be over $20,000, and replacing a water-soaked gym setup may cost even more. In contrast with those amounts, the average premium for attaching a home gym endorsement or rider—usually under $200 per year—is well worth the peace of mind.

Consequences of not having insurance:

- Loss of thousands from theft or catastrophe.

- Payment of medical expenses and lawsuits out-of-pocket.

- Rejection of claims from standard policies due to exclusions.

- Delays in equipment replacement without evidence or coverage.

Peace of Mind Is Priceless:

With your home gym securely insured, you can worry less about “what if” situations whenever you invite over a workout session or invest in new equipment. You get to concentrate on what truly matters: your fitness, well-being, and healthy workouts.

Advantages of Insurance for Home Gym:

- Complete reimbursement for lost or damaged equipment.

- Legal protection in case anyone gets hurt.

- Customized coverage to suit your individual setup and use.

- Peace of mind in managing unforeseen occurrences.

Final Thoughts: Protect What Powers Your Progress

Having a home gym is not just a convenience—it’s a valuable investment in your long-term well-being, personal development, and daily productivity. If you’ve equipped a spare room with dumbbells and resistance bands or constructed a full-scale training center in your garage, your equipment warrants the same care as any other valuable asset. But like any worthwhile investment, it has its risks. From electrical malfunctions and water leaks to accidental trauma and liability issues, the risks to your fitness facility are all too real and frequently underappreciated.

As we delve into throughout this article, it’s possible to be left vulnerable by counting on mere standard homeowners’ insurance. The majority of insurance policies have strict caps on personal property, and hardly any take into account the special challenges provided by fitness equipment, particularly in business contexts. That’s why taking steps to get the correct insurance for home gym installations isn’t merely prudent—it’s imperative to enjoy prolonged peace of mind.

By reviewing your current coverage, documenting your equipment, and exploring specialized options like equipment breakdown protection or business liability insurance, you’re creating a financial safety net around your gym. Real-world scenarios have shown just how quickly unexpected events can turn costly—and how much relief proper insurance can provide in those moments.

Don’t wait for a flood, accident, or lawsuit to learn the hard way. Call your Insurance for Home Gym company today, read your policy thoroughly, and request custom options that fit your specific home gym configuration. Whether you’re hoisting heavy weights, instructing clients, or just getting a daily workout in, ensure you’re covered—every rep, every step, every session—with the appropriate Insurance for Home Gym

Also Read: Home Insurance McAllen TX: 5 Powerful Reasons You’re Paying Too Much

Frequently Asked Questions (FAQs)

Is my Insurance for Home Gym covered under standard homeowners insurance?

Not always. Most homeowners policies offer limited coverage for personal property, but high-value fitness equipment may exceed those limits. You may need additional endorsements or a scheduled personal property rider to fully cover your home gym setup.

Do I need separate Insurance for Home Gym?

If you’ve invested significantly in equipment or use the space for training others, then yes. Insurance for home gym setups ensures protection against theft, damage, and liability, which standard homeowners insurance might not fully cover.

What happens if someone gets injured in my home gym?

If you don’t have adequate liability coverage, you could be held personally responsible for medical bills or legal costs. To protect yourself, add personal liability or umbrella coverage to your policy, especially if guests or clients use your gym.

How much does Insurance for Home Gym cost?

Costs vary depending on your equipment value and the type of coverage. A simple rider might cost $100–$200 annually, while business-related insurance could be higher. It’s best to consult your insurer for a custom quote.

Is business use of a home gym covered under homeowners insurance?

No. If you’re using your home gym for paid training, group sessions, or client visits, you’ll need a home-based business policy or commercial liability insurance. Standard homeowners coverage excludes business activities.

Can I insure individual gym equipment like a treadmill or stationary bike?

Yes, you can. If your equipment is high-value (like a Peloton, NordicTrack, or Technogym unit), you can schedule it individually on your homeowners policy or get equipment breakdown coverage. This ensures you’re reimbursed for damage, malfunction, or theft.

Does renters insurance cover my home gym equipment?

Renters insurance may provide limited coverage for personal property, but like homeowners insurance, it often has sub-limits. If you rent and own expensive gym gear, consider increasing your personal property limits or getting additional endorsements.

What documents do I need to file a claim for gym equipment?

You’ll need:

1. Purchase receipts or invoices.

2. Photos or videos of the damaged or stolen items.

3. A copy of your inventory list.

4. A police report (for theft-related claims).

5. Proof of ownership (warranty, manuals, serial numbers).

Keeping digital backups of all documents is highly recommended.

Will my insurance cover outdoor gym equipment?

Most insurance companies only cover gym equipment kept inside your home or garage. Outdoor equipment, such as in backyard gyms or patios, may not be covered unless explicitly stated in your policy. Talk to your insurer to include it if needed.

Is flood or water damage to my home gym covered?

Not by default. Standard homeowners policies typically exclude flood damage. If your gym is in a basement or flood-prone area, consider purchasing separate flood insurance through the National Flood Insurance Program (NFIP).

Can I claim wear and tear on gym equipment?

No, insurance won’t cover normal wear and tear or depreciation. However, equipment breakdown coverage might cover unexpected mechanical or electrical failures, depending on your policy.

One Comment