Home Insurance McAllen TX: 5 Powerful Secrets

Home insurance McAllen TX is crucial to protecting your home against unanticipated damage, natural catastrophes, theft, and claims of liability. Residing in an area like McAllen—where weather-related events like hailstorms and flooding are not unusual—makes it more than a good idea to have a trustworthy home insurance; it’s a financial imperative. But what if you unknowingly pay way too much for it? Most homeowners stick with old policies or accept whatever first quote they get without knowing they might be overlooking superior coverage and substantial savings.

Whether buying a policy for the first time or renewing one you’ve held for years, knowing what really determines the price of home insurance in McAllen TX can mean making wiser monetary decisions. Rates are highly variable based on where your house is, how old it is, its condition, and even the materials it was built from. That’s not all, though—some policyholders fall prey to expensive traps such as overlooking discounts, underestimating risk areas, or remaining with the same company out of custom.

In this article, we’ll take seven strong reasons you might be overpaying for your policy and present simple, actionable steps to reduce your premiums without sacrificing your cover. From policy mismatches to regional risk factors and sneaky charges, this article is designed especially for McAllen homeowners. If you’re ready to gain control of your home insurance and keep money in your pocket, let’s get started.

Table of Contents

1. You’re Not Shopping Around for Better Rates-Home Insurance McAllen TX

The Problem with Loyalty:

One of the most frequent errors made by homeowners is remaining with one and the same insurer for years without shopping around for new quotes. Although this might appear as a gesture of loyalty, it usually turns sour because of a pricing tactic called price optimization. Insurers study customer behavior and realize that long-term customers are not likely to jump ship—so they gradually raise your premiums year after year, even if your risk profile has not changed.

This holds particularly in areas such as McAllen, whose housing markets and environmental risk factors fluctuate dramatically. Consequently, most people find themselves paying more for home insurance McAllen TX merely because they haven’t compared to see if there are any better offers.

Tips to Save:

- Ask for quotes from at least three different companies every year to compare coverage, charges, and deductible choices.

- Use online resources such as Policygenius and The Zebra to make the process easier. These websites enable you to compare hundreds of highly rated companies that provide home insurance McAllen TX policies.

- Don’t be afraid to call your present insurer and request a rate match if you get a lower quote somewhere else. Most companies will lower your premium to retain your business.

By doing your shopping around every year, you drive competition among providers—and that places you in charge of your premium instead of being a victim of year-to-year hikes.

Local Insurance Brokers Can Help:

Another underutilized strategy is doing business with local insurance agents in McAllen, as opposed to just going with well-known national providers. Independent agents handle the home insurance McAllen TX business and are familiar with the city’s distinct perils, such as flooding from the Rio Grande, hail storms, and high wind events typical of South Texas.

National insurance companies can use wide risk profiles that don’t accurately depict McAllen’s conditions today. Local brokers, on the other hand, can assist you in developing a tailored policy that best suits your home’s unique needs without paying extra for redundant add-ons.

Bullet Advantages of Working with Local Agents:

- Individualized Service: You’ll have a personal representative who understands you and your house—not a generic agent in a call center.

- Personalized Policy Recommendations: Based on your ZIP code, home age, materials, and flood risk level.

- Simplified Claims Process: Local agents can guide you through claims and even negotiate directly with adjusters on your behalf.

Example: A homeowner in the 78504 ZIP code saved more than $600 a year by switching from a national brand to a McAllen-based broker who tailored their policy after a property reinspection.

To begin with, browse for reputable brokers via the Texas Department of Insurance or check on Yelp McAllen Insurance Listings for customer-rated agencies.

Briefly, home insurance McAllen TX is not an off-the-rack proposition. Shopping for rates and consulting local professionals are two of the strongest weapons to help you avoid overpayment.

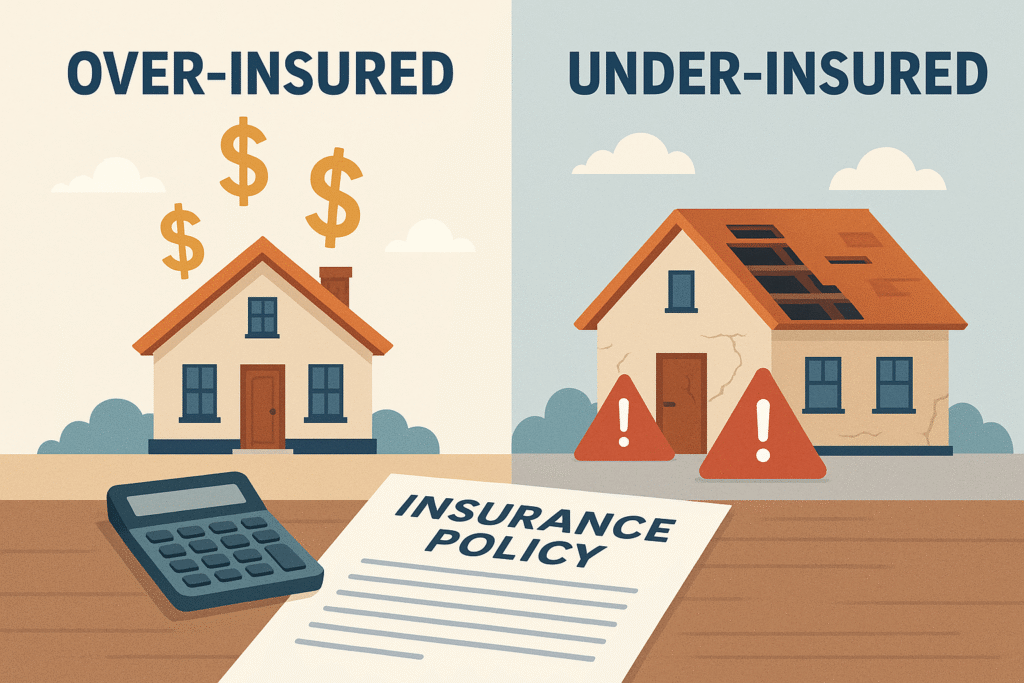

2. You’re Over-Insured or Under-Insured- Home Insurance McAllen TX

Confusing Market Value with Replacement Cost:

One of the most costly mistakes homeowners make when purchasing home insurance McAllen TX is confusing a property’s market value with its replacement cost. While the market value reflects what your home would sell for—including the land—it’s not the figure insurers use to calculate how much it would cost to rebuild your house in case of a disaster. Covering your house for its full market value means that you’re most likely overpaying, particularly because land doesn’t burn down, flood, or collapse.

Replacement cost, however, pays for the actual cost of rebuilding your house with comparable materials and workmanship minus the value of the land. This is what you should cover for, and this typically translates to a more realistic—and often lower—premium.

Real Example:

A homeowner in North McAllen had a home with a market value of $280,000. Having consulted a local agent, they found that the actual replacement cost was just $200,000. By modifying coverage to this extent, they reduced their premium by almost $500 per year.

To make an estimate of your home’s replacement value, utilize tools made available by your insurer or local appraisers. The Insurance Information Institute (III) also has tips on how to calculate proper coverage.

Ignoring Personal Belongings Coverage:

When you buy home insurance McAllen TX, it’s not only the house building you’re covering—it’s all the stuff within as well. Most homeowners either undervalue their properties or overvalue them, which can lead to either insufficient coverage after a loss or too expensive premiums.

What Can Go Wrong:

- Under-insuring: You lose $25,000 worth of electronic and furniture in a fire, but your coverage limits $15,000.

- Over-insuring: You pay premiums for $100,000 of contents when you have only $40,000 worth of items.

Tips to Ensure Accuracy:

- Make a digital list of all substantial items. Make note of serial numbers, receipts, and store photos safely in the cloud or with your agent.

- Utilize home inventory apps such as Sortly or Encircle to simplify and organize this task.

- Review your personal property coverage annually, particularly after acquiring new electronics, jewelry, or furniture.

Extra Tip:

Remember that valuable items such as art, watches, or collector items can necessitate regular personal property endorsements. Failing to do so could mean loss limits that are far below the value of your items.

Selecting the proper amount of coverage on your home and property is the key to paying no more than you need to, or facing an unexpected deficiency when loss occurs. If you’re renewing an existing policy, or purchasing your first, reviewing your coverage levels closely is a requirement when searching for home insurance McAllen TX.

3. You Haven’t Taken Advantage of Available Discounts- Home Insurance McAllen TX

Common Discounts You Might Be Missing:

If you’ve not looked at your policy in a while, you could be leaving cash on the table. A great number of homeowners in McAllen are eligible for all types of home insurance discounts, but they don’t know or don’t ask. Insurance companies often don’t promote these discounts so knowing what to ask can be a big money-saver.

If you are looking for home insurance McAllen TX, it is important to understand that your discount eligibility can lower your premium by a great deal—often up to 25%.

Most Often Overlooked Discounts:

- Bundling Discount – Bundle your home and auto policies with the same company for as much as 20% off. Progressive, Allstate, and State Farm are some of the companies providing bundling discounts in McAllen.

- New Roof Discount – If your roof has recently been replaced in the past 5–10 years, you could be eligible for reduced premiums. Insurers consider new roofs to be lower risk for wind and water damage.

- Smart Home Device Discount – By installing smart smoke detectors, leak sensors, or security cameras, you can prevent losses and become eligible for smart tech rebates.

- Claims-Free Discount – Never made a claim in the last 3–5 years? You can save as much as 10%.

- Senior Citizen Discount – Homeowners aged 55 and above can expect to enjoy a discount as they exhibit fewer risky behaviors such as being home more often and improved maintenance habits.

These reductions are not automatic—you must request them and present evidence if required. This holds particularly in markets such as McAllen, where houses are of different ages and types, and premiums are influenced by both local hazards and specific property characteristics.

How to Ask the Right Questions:

Whether you are renewing a current policy or obtaining a new quote, being proactive will pay dividends. Most carriers will not go through all available discounts with you unless you request it.

Ask These Questions When You Get a Quote:

- “What home insurance McAllen TX discounts do I qualify for?”

- “Will my new security system or smart thermostat lower my premium?”

- “How much can I save by combining with my car insurance?”

- “Do I receive any discounts for loyalty or renewal?”

- “Can I obtain a lower premium with a higher deductible?”

Pro Tip:

To become eligible for additional discounts, make some cost-effective home safety improvements:

- Install smoke and carbon monoxide alarms in all main rooms.

- Have deadbolt locks on all outside doors.

- Utilize motion-sensing lights and monitored alarm systems.

- Install water leak sensors close to appliances such as dishwashers and water heaters.

Even minor improvements can have a large impact on your home insurance McAllen TX rates. And many upgrades not only reduce premiums but also prevent expensive damage—saving you even more down the line.

For additional types of discounts and requirements to be eligible, visit the Texas Department of Insurance which offers in-depth guides and policy comparisons.

4. You’re Not Accounting for McAllen-Specific Risks- Home Insurance McAllen TX

Texas Weather and Your Premium:

McAllen, Texas, sits in the southernmost region of the state and experiences a wide range of severe weather patterns that significantly influence home insurance McAllen TX premiums. From hailstorms and hurricanes to unexpected flash flooding, the risk of natural disasters is notably higher in this region than in many other parts of Texas. If your policy doesn’t accurately represent these threats, you might either be paying too much for unnecessary coverage—or worse, not enough when disaster hits.

Local Insight:

In 2020, Hidalgo County (McAllen’s location) had several intense hailstorms that caused more than $40 million in property losses. Most homeowners didn’t renew their policies after these occurrences, only to find that their claims didn’t cover them as much as they thought. This highlights the need to match your policy with current risks.

Insurers keep a close eye on local climate trends, and if your house is in a high-risk area, they’ll include that in your premium. But if your house has protective features—such as impact-resistant roofs or storm shutters—you can qualify for rate discounts, so it’s worth mentioning to your insurer.

For additional information about Texas climate trends and how they influence insurance, go to the Texas State Climatologist website.

Flood Insurance Is Separate:

One common misconception that homeowners shopping for home insurance McAllen TX make is assuming that flood damage falls under their standard policy. It doesn’t.

Flood insurance has to be bought as a separate entity, most commonly through the National Flood Insurance Program (NFIP), which is underwritten by FEMA. This is especially true in McAllen, where heavy downpours and inadequate drainage can lead to flash floods even outside of designated flood zones.

Tips to Stay Protected:

- Use FEMA’s Flood Map Service Center (msc.fema.gov) to see if your house is located in a high-risk flood zone.

- Even if you’re not in a high-risk area, 25% of flood claims arise from low-to-moderate risk areas, says FEMA.

- Consider adding excess flood insurance if your house is very valuable or sits in a repetitive loss area.

Additional Tip:

If you’re in a high-risk flood zone and have a mortgage, the lender might legally require you to carry flood insurance. However, even if the law has no such requirement, you could save yourself tens of thousands of dollars in case a flood occurs.

Don’t assume you’re fully protected—read your declarations page carefully, and speak with your insurance agent to confirm your flood risk coverage. Many residents searching for home insurance McAllen TX often overlook this crucial aspect, leading to devastating financial consequences when flooding occurs.

Knowing about McAllen-specific environmental hazards means your policy really covers your house, not just on paper but when you can least afford it. Current, risk-based coverage can keep you ready—and save you money when preventative efforts are deployed.

5. You Haven’t Reassessed Your Deductible-Home Insurance McAllen TX

Low Deductibles Mean Higher Premiums:

Selecting a low deductible can appear to be a good idea when buying home insurance McAllen TX—particularly if you are concerned about surprise out-of-pocket expenses. However, in reality, this will add up to a huge increase in your premium every year.

A deductible is how much you consent to pay out-of-pocket before your insurance begins. The lower your deductible, the more the insurer assumes risk, and they compensate by charging you more for premiums. Most homeowners in McAllen simply use the standard $500 deductible out of convenience, but this could end up costing them a lot of extra money every year.

Tip to Save:

Consider boosting your deductible to $1,000 or even $2,500 if you have an emergency savings fund on hand. It would cut your premium by 15% to 25% a year, depending on your insurer.

For more information, read this Forbes guide to selecting home insurance deductibles, which explains the financial trade-offs and dollars at stake.

Real Example:

A homeowner in McAllen who paid $1,600/year with a $500 deductible raised his deductible to $1,500 and reduced his premium to $1,275—a savings of $325 per year.

Separate Deductibles for Wind/Hail:

Another commonly neglected aspect of home insurance McAllen TX policies is the existence of divisible deductibles for wind and hail losses. With the climate in McAllen and its more-than-frequent severe weather occurrences, insurers usually bifurcate the deductibles: one for general perils and a higher deductible for windstorm or hail-related claims.

This implies you might have a standard $1,000 deductible but a 2% wind/hail deductible—based on a percentage of the insured value of your home. For a $250,000 house, that’s $5,000 out-of-pocket before your insurance kicks in on wind or hail damage.

Tips for McAllen Homeowners:

- Review your declarations page to determine if you have stand-alone wind/hail deductibles.

- Use percentage deductibles only if your house is relatively new, well-serviced, and built with storm-resistant materials.

- If you reside in an older house, make a flat dollar deductible a consideration, even if the premium is slightly higher, to prevent high out-of-pocket expenses following a storm.

For information on how to read deductibles in Texas, see the Texas Department of Insurance: Understanding Your Policy page.

Reevaluating your deductible on a yearly basis is an intelligent strategy to balance cost and risk. For homeowners looking for cheap yet efficient home insurance McAllen TX, strategically adjusting deductibles is one of the fastest means to manage premium expenses without lowering quality coverage.

Final Thoughts-Home Insurance McAllen TX

When it comes to safeguarding your home, home insurance McAllen TX is not only a financial or legal requirement—it’s a critical protection against the unpredictable. Yet many homeowners in McAllen overpay unnecessarily due to outdated policies, false coverage, or lost opportunities for savings.

In this manual about Home Insurance McAllen TX, we revealed 5 strong explanations why your premium could be too expensive and gave practical steps to correct it—from comparing rates and rethinking deductibles to learning regional threats such as hail and flooding. You’re either a new homeowner or policy re-newer looking to make informed changes. Either way, taking the time to scan your insurance can result in improved coverage and decreased expense.

It’s time to be in charge. Reach out to area brokers, comparison shop, and read your policy line by line. The better you’re informed, the more control you have to tailor a plan that meets your requirements—without breaking the bank.

Act now: Check out your existing coverage, get quotes from multiple sources, and ensure your home insurance McAllen TX actually works for you—rather than against your checkbook.

Also Read: Home Insurance Portugal: 7 Shocking Truths Every Homeowner Must Know

Frequently Asked Questions (FAQs)

What is the average cost of Home Insurance McAllen TX?

The average cost of home insurance McAllen TX ranges from $1,200 to $1,800 per year, depending on factors such as home size, construction materials, deductible, and coverage limits. Premiums are also influenced by local weather risks like hailstorms and flooding.

Does homeowners insurance in McAllen cover flood damage?

No. Standard home insurance McAllen TX policies do not cover flood damage. You must purchase a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

Can I save money by bundling my home and auto insurance?

Absolutely. Bundling your home and auto insurance with the same provider can lead to savings of up to 20% on your premiums. Be sure to ask your provider for bundling options.

How often should I reassess my home insurance policy?

Experts recommend reviewing your policy once a year, especially if you’ve renovated your home, purchased expensive belongings, or experienced changes in local risk factors. This ensures your home insurance McAllen TX coverage stays aligned with your current needs.

What’s the difference between market value and replacement cost in home insurance?

Market value includes the land and location—replacement cost focuses only on rebuilding the structure. For home insurance McAllen TX, always insure your home based on replacement cost to avoid overpaying for unnecessary land coverage.

Are there any discounts available for smart home upgrades?

Yes. Installing smart security systems, leak detectors, and smoke alarms can qualify you for discounts of 5%–10% with many insurers offering home insurance in McAllen.

One Comment