Home Insurance Portugal: 7 Shocking Truths You Must Know

Home insurance Portugal is not merely a monthly expense—it’s an essential bulwark that protects your home, personal items, and financial health. You might be a native-born local or an expat who’s bought a dream house in Lisbon, Porto, or picturesque Algarve countryside, but either way, it’s all about having the right policy in place. With proper coverage, you can shield yourself against unforeseen catastrophes such as fire, water damage, burglary, and even lawsuits—saving you thousands of euros and providing peace of mind during uncertain times.

Even with its increasing need, it still surprises many homeowners how the key components of home insurance Portugal work. From legal requirements and supplementary coverage to exclusions in the policy and premium volatility, the fine print is full of surprises. Others assume they’re completely insured when they’re not, while others neglect cost-cutting measures such as bundling or risk assessment. In this article, we expose 7 startling facts every homeowner ought to know—facts that can assist you in making wiser, safer, and more economical choices regarding insuring your home in Portugal.

Table of Contents

1. Home Insurance Portugal is Not Always Mandatory—But It Should Be

When Home Insurance Is Required by Law:

Although home insurance Portugal isn’t mandatory for every homeowner at all times, there are certain situations when it becomes a mandatory requirement by law.

- Mortgage Requirement: When you buy a property in Portugal on a mortgage basis, you are by law compelled to obtain insurance against damage by fire. It is a requirement imposed by Portuguese banking and insurance laws for the lender’s and borrower’s protection in the event of accidental property destruction. Without the same, your loan may not be approved or may get delayed.

- Condominium Rules: If your property is part of a shared building, such as an apartment in Lisbon or a condo in Porto, the condominium’s administrative entity may impose a collective insurance policy. This policy often covers common areas like staircases, elevators, and the building structure. However, individual units may still require separate coverage for contents and personal liability.

You can check for legal guidelines about property and insurance responsibilities on the official government portal ePort Portugal.gov.pt, which is available at the disposal of citizens and residents for facilitating administration procedures in Portugal.

Why You Should Still Get It:

Unless your type of insurance is required by law, home insurance Portugal is a very responsible and financially prudent choice to make regarding your particular type of property. Here’s why:

- Natural Disasters: Portugal is susceptible to fires, particularly in central and southern parts of the country in the summer. Coastal and riverbank areas, such as districts within Porto and Coimbra, are also becoming subject to seasonal flooding. Furthermore, areas such as the Azores and Lisbon are earthquake-prone, exposing houses to earthquakes.

- Urban Crime Risks: City centers like Lisbon and Faro saw a consistent increase in burglaries and thefts, especially in tourist areas. In case something is stolen or lost, not having coverage can be an expensive gamble to replace what is gone.

- Liability Expenses: Things do go wrong. When a pipe bursts and causes water damage to your neighbor’s apartment or a visitor hurts themselves on your premises, liability claims can quickly soar into thousands of euros. With the proper home insurance Portugal policy, legal and compensation expenses may be covered.

Tip: Always check with your mortgage lender, property agent, or condominium association to confirm if home insurance Portugal is mandatory for you. It also never hurts to check with certified insurers or independent advisors.

For current regulatory needs and homeowner information, the Autoridade de Supervisão de Seguros e Fundos de Pensões (ASF) is another valuable government resource. They regulate the insurance market in Portugal and offer consumer guides for selecting proper coverage.

2. Basic Coverage Often Isn’t Enough

What Basic Policies Typically Cover:

From a glance, basic home insurance Portugal policies appear to be all-encompassing. Most basic plans are meant to provide basic protection against everyday hazards and risks, but that protection is not usually comprehensive. Generally, a typical policy in Portugal will have:

- Fire and Smoke Damage: This is the most basic coverage, particularly in the case of a mortgaged home. Fire coverage is a requirement by law in most Portuguese mortgage contracts.

- Storms and Natural Disasters: Damage coverage in the case of heavy rainfall, hail, windstorms, and snow is generally covered—but subject to certain conditions.

- Burglary or Theft: Although a few policies cover it, it’s mostly an optional rider. Always confirm if burglary protection is on and under what circumstances.

- Third-Party Liability for Injuries: This addresses cases where a person gets hurt in or on your property as a consequence of your negligence, e.g., a guest falling on your staircase.

You can check out samples of what’s generally in a standard policy from companies like Fidelidade and Zurich Portugal, both of which offer online quotes and flexible plans.

Shocking Gaps in Basic Coverage:

Even if many homeowners think that standard home insurance Portugal policies usually have all the necessary protections, they frequently do not. Gaps in coverage can lead to crippling out-of-pocket costs if disaster happens.

- No Flood Coverage Unless You Ask: Standard policies do not usually cover damage from floods brought about by overflowing rivers, flash floods, or drainage system failures. If you reside near rivers such as the Douro, Mondego, or Tagus, this is a critical omission.

- Earthquake insurance not included: Portugal is prone to seismic activity, but particularly so in Lisbon and the Azores. Earthquake insurance is not part of the standard coverage and is taken separately.

- Items of value not comprehensively insured: High-cost electronics, watches, artwork, or antiques are typically limited to low value unless you specify otherwise and individually insure them. Most homeowners incorrectly believe comprehensive coverage with actual limits being very restrictive.

These exclusions can leave you financially exposed, particularly if your property sits in higher-risk areas such as the Madeira or Douro Valley, where weather extremes and geological hazards are a frequent occurrence.

Tip: Get a clear breakdown of what is—and isn’t—insured before you buy a policy. Ask your insurer about add-ons that suit your region’s risk profile and the value of your property.

Leading insurers such as Tranquilidade and Ageas Seguros also offer multi-risk and customizable insurance packages tailored to your property type and location.

Taking the time to review these options ensures that your home insurance Portugal policy provides true peace of mind—not just a false sense of security.

3. Prices Vary Widely Based on Location and Property Type

How Insurers Calculate Premiums:

Home insurance Portugal cost is based on a number of critical considerations. Understanding what affects your premium can save you money while maintaining adequate coverage.

- Location: Properties in coastal resorts such as Cascais, Faro, and Lagos tend to have more expensive premiums because of exposure to dangers like storms, flooding, and burglary. Conversely, inland or low-risk regions might qualify for reduced rates.

- Age and Condition: Older homes with old systems are more likely to be damaged and are more expensive to insure. New or newly remodeled houses can be eligible for discounts—particularly if you can provide proof of inspection or remodeling.

- Building Materials: Homes made of concrete or brick are less expensive to insure because they are more durable.

- Security Measures: Installing alarms, CCTV and extra-strong doors can pay off in terms of lower premiums. Insurers pay lower-risk properties a better rate.

Real Example of Price Variance:

| Property Type | Location | Monthly Premium (Est.) |

|---|---|---|

| Modern Apartment | Lisbon | €12–€20 |

| Traditional Cottage | Algarve | €25–€40 |

| Villa with Pool | Cascais | €45–€60 |

Tip: Install smoke detectors and burglar alarms to reduce your premium by up to 15%.

Use price comparison tools like ComparaJá.pt to find affordable policies.

Wooden homes tend to be pricier because of the risk of fire and pests.

4. You May Be Underinsured Without Realizing It

The Risk of Underestimating Your Property Value:

One of the home insurance Portugal most underappreciated concerns is under-insurance—the situation in which the amount covered does not exactly align with the actual cost to reconstruct or rebuild your property. An error often made is insuring a house on market value instead of reconstruction cost.

- Market Value encompasses the land, site, and market conditions, which are not applicable to insurance since land is not susceptible to destruction.

- Reconstruction Cost is based on what it would take to rebuild your house from scratch, including materials, labor, permits, and architectural fees.

This is an important distinction. For instance, a Lisbon city center home might be highly valued for the property it sits on, but rebuilding it if it were destroyed in a fire could cost substantially less—or more—based on its form and materials.

Home insurance Portugal companies require true valuations when they issue policies. If your policy is drawn up using low or incorrect values, you may not receive sufficient payment when you most need it.

Consequences of Underinsurance:

If you do not insure your home properly, you can face serious financial and legal problems:

- Partial Payouts: If your amount of insurance is inadequate, your insurer might only pay for some of your damages, requiring you to pay the balance.

- Delays in Rebuilding: Insufficient funds can lead to very long delays, particularly when reconstruction expenses increase after a catastrophe.

- Legal Conflicts: Differences between declared and actual values can result in claim disputes or even denial of claim.

For instance, after the 2017 wildfires in Central Portugal, some homeowners discovered too late that their policies did not encompass true rebuild costs—subjecting them to financial strain and extended housing insecurity.

Tip: Always request your insurer to perform or sign off on a professional property valuation prior to setting your coverage amount. Alternatively, employ a certified property assessor for an unbiased report.

Companies like Deco Proteste provide consumer-friendly guides and resources for Portuguese homeowners to calculate correct insurance values and avoid expensive mistakes.

Being properly covered means home insurance Portugal really delivers when it counts—giving full protection, quicker recovery, and enduring peace of mind.

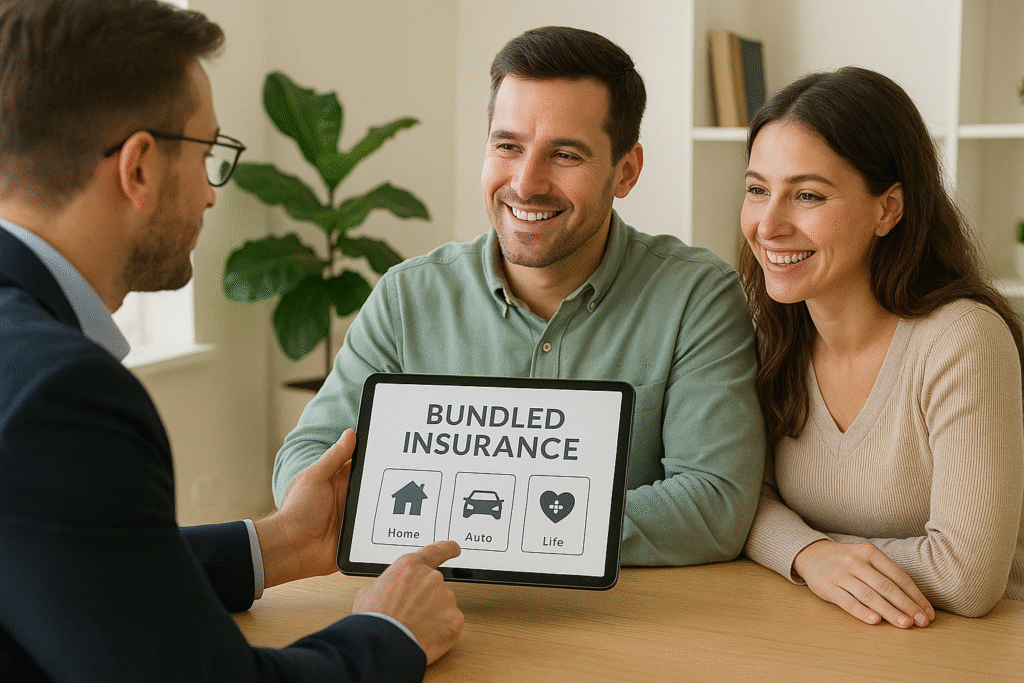

5. Bundling Policies Can Save You Hundreds: Home Insurance Portugal

The Benefits of Combining Home and Auto Insurance:

When buying home insurance Portugal, most individuals ignore a strong money-saving technique—bundling. This involves linking two or more insurance policies (such as home, car, or life) with the same insurer to get considerable discounts and increased convenience.

Bundling has several benefits:

- Discounted Premiums: Most insurers provide 10–20% discounts when you bundle home and automobile insurance.

- Simplified Management: One insurer streamlines your payments, one bill, and one renewal date, making it simpler to manage your insurance requirements.

- Improved Customer Support: It is easier to experience service from one insurer and also gets you the claims faster.

Firms such as Fidelidade, Ageas Seguros, and Liberty Seguros in Portugal provide bundle discount if you purchase home insurance Portugal along with other products.

Where to Find Bundle Deals:

Not all bundles are equal. This is what you should look for:

- Flexible Coverage: Select bundles that offer variable limits for home and auto.

- Clear Terms: Steer clear of surprise charges or terms that bind you for many years.

- Seasonal Offers: Insurers tend to offer limited-time discounts or bonuses, e.g., gift cards or roadside assistance for free.

| Provider | Bundle Offer | Extra Benefits |

|---|---|---|

| Fidelidade | 15% off home + auto | Emergency assistance |

| Liberty Seguros | Multi-policy discounts | Single customer portal |

| Ageas Seguros | Flexible mix of home, auto, and life plans | Travel insurance add-ons available |

Use a comparison site like ComparaJá.pt to evaluate bundled plans and choose the one that fits your lifestyle and budget.

Choosing to bundle is not just about savings—it’s about simplifying your financial life while ensuring your home insurance Portugal policy remains both comprehensive and cost-effective.

6. Claims Process Can Be Frustrating Without Documentation

What You Need to File a Claim: Home Insurance Portugal

Making a claim on your home insurance Portugal policy can be seamless—or immensely frustrating—depending on how prepared you are. Most claim denial or delay is caused by missing paperwork, unclear reports, or policy misconceptions. Here’s what is usually needed:

- Photographic Evidence: Good quality photos or videos of the damage right after the incident.

- Police Report: Required for theft, vandalism, or third-party damage.

- Receipts or Invoices: Evidence of purchase for stolen or damaged goods.

- Insurance Policy Document: Your coverage information and policy number will be required while processing your claim.

Having these on hand can greatly accelerate your claim and get you reimbursed adequately.

Why Claims Get Denied in Home Insurance Portugal:

Although you believe you have coverage, there are a number of reasons your home insurance Portugal claim can be denied or downgraded:

- Late Notice: Claims should typically be reported within 8 days of the occurrence (refer to your individual policy).

- Inadequate Documentation: Lost receipts or vague descriptions undermine your claim.

- Coverage Exclusions: Numerous policies exclude certain events unless otherwise added—such as floods, earthquakes, or mold.

- Misrepresentation: Incorrect information on your application may invalidate your claim entirely.

One typical situation is when homeowners receive payment for water damage claims only to find that their policy excludes burst pipes or mold due to lack of maintenance.

The ASF (Autoridade de Supervisão de Seguros e Fundos de Pensões) annually receives hundreds of complaints concerning refused or delayed claims—largely because of misinterpretation of policy terms or incorrect filing.

Tip: Save digital versions of all documents—photos, bills, and policy information—on cloud storage or email. This way, you can access them in an instant when required.

You can also get consumer-friendly claim guides from Deco Proteste, which details step-by-step how to make successful home insurance claims in Portugal.

By being properly organized and well-informed, you make your home insurance Portugal policy truly serve you—when you most need it.

7. Earthquake and Flood Coverage: A Must-Have Add-On

Why Standard Policies Exclude These Events:

While Portugal enjoys a pleasant climate and stunning scenery, it also suffers from severe natural threats. Yet most standard home insurance Portugal policies do not cover these events—two of the most expensive hazards.

- Earthquakes: Portugal is located on a seismically active area, more so in cities such as Lisbon and the Azores. The catastrophic 1755 earthquake of Lisbon is a historical marker of how severe the danger can be. Notwithstanding this, earthquake coverage is generally excluded and has to be added as an individual rider.

- Flooding: As extreme weather has increased, cities such as Lisbon, Coimbra, and Porto have seen serious flash flooding in the past few years. Overflows of rivers, storms, or drainage are typically not covered in standard plans unless you pay extra.

Omitting these extras may mean you will be paying through the nose to fix damage that costs tens of thousands of euros.

Real Example of Natural Disaster Impact: Home Insurance Portugal

In 2022, torrential floods in Lisbon destroyed hundreds of homes, stores, and cars. Hundreds of homeowners learned too late that their home insurance Portugal policies did not cover claims related to floods. The result? Sustained delays in reconstruction, legal battles with insurers, and colossal personal losses.

Another illustration: residents of São Miguel (Azores) were struck by an earthquake in 2023 and could only recover damages if they had specifically chosen earthquake coverage—emphasizing the essential necessity of region-specific coverage.

How to Get Protected:

Leading insurers like Fidelidade, Tranquilidade, and Zurich Portugal offer customizable plans where flood and earthquake coverage can be added based on your location and risk level.

| Add-On | Estimated Monthly Cost | Recommended If You Live In |

|---|---|---|

| Earthquake Cover | €2–€5 | Lisbon, Azores, Algarve |

| Flood Protection | €3–€7 | Porto, Coimbra, areas near rivers/coasts |

Tip: Check your local municipality’s flood and seismic risk maps or use the IPMA (Portuguese Institute for Sea and Atmosphere) to evaluate your area. Then, discuss risk-specific add-ons with your insurer.

Don’t assume your standard home insurance Portugal policy covers all catastrophes. Proactively adding flood and earthquake coverage could be the smartest financial move you make.

Final Thoughts: Home Insurance Portugal

Understanding home insurance Portugal is essential for protecting not only your property but your financial stability and peace of mind. While many believe a standard policy is enough, we’ve uncovered seven shocking truths—from gaps in coverage and regional risk factors to under-insurance and claim pitfalls—that prove otherwise.

Whether you live in Lisbon, own property in the Algarve, or are a homeowner in the Azores, checking your policy terms and adjusting your cover is essential. Don’t wait until something goes wrong to realize you’re not completely covered.

Act now:

- Compare suppliers such as Fidelidade, Zurich Portugal, and Tranquilidade.

- Utilize tools such as ComparaJá.pt to find the best deal.

Discuss this with your bank, property owner or a qualified advisor to make sure your policy matches your real needs.

Your home is one of your most expensive assets—be sure that your home insurance in Portugal is designed to safeguard it.

Also Read: Home Insurance Construction Type: 10 Crucial Facts Most People Miss

Frequently Asked Questions (FAQs)

Is home insurance mandatory in Portugal?

Not always. However, home insurance Portugal is required if you have a mortgage (fire coverage is mandatory) or live in a condominium where building insurance may be imposed.

What does basic home insurance in Portugal usually cover?

Typically, it includes fire, storms, and third-party liability. However, burglary, floods, and earthquakes are usually optional add-ons.

How much does home insurance cost in Portugal?

Premiums range from €10 to €60 per month, depending on your home’s location, size, age, construction, and added coverage.

What’s the difference between market value and reconstruction cost?

Market value includes the land and location value, while reconstruction cost refers only to the cost to rebuild the home. Insurance should be based on reconstruction cost.

Can I get discounts on home insurance in Portugal?

Yes! You can save by bundling your home insurance Portugal with auto or life insurance. Installing security systems can also lower premium

What should I do if my claim is denied?

First, review your policy terms. Then contact your insurer for clarification. If needed, file a complaint with the ASF, the Portuguese insurance regulator.

How do I know if I need flood or earthquake coverage?

If you live near water (like in Porto or Coimbra) or in a seismic zone (Lisbon or Azores), you should consider adding this protection to your policy

One Comment