Why Home Health Workers Compensation Insurance Matters?

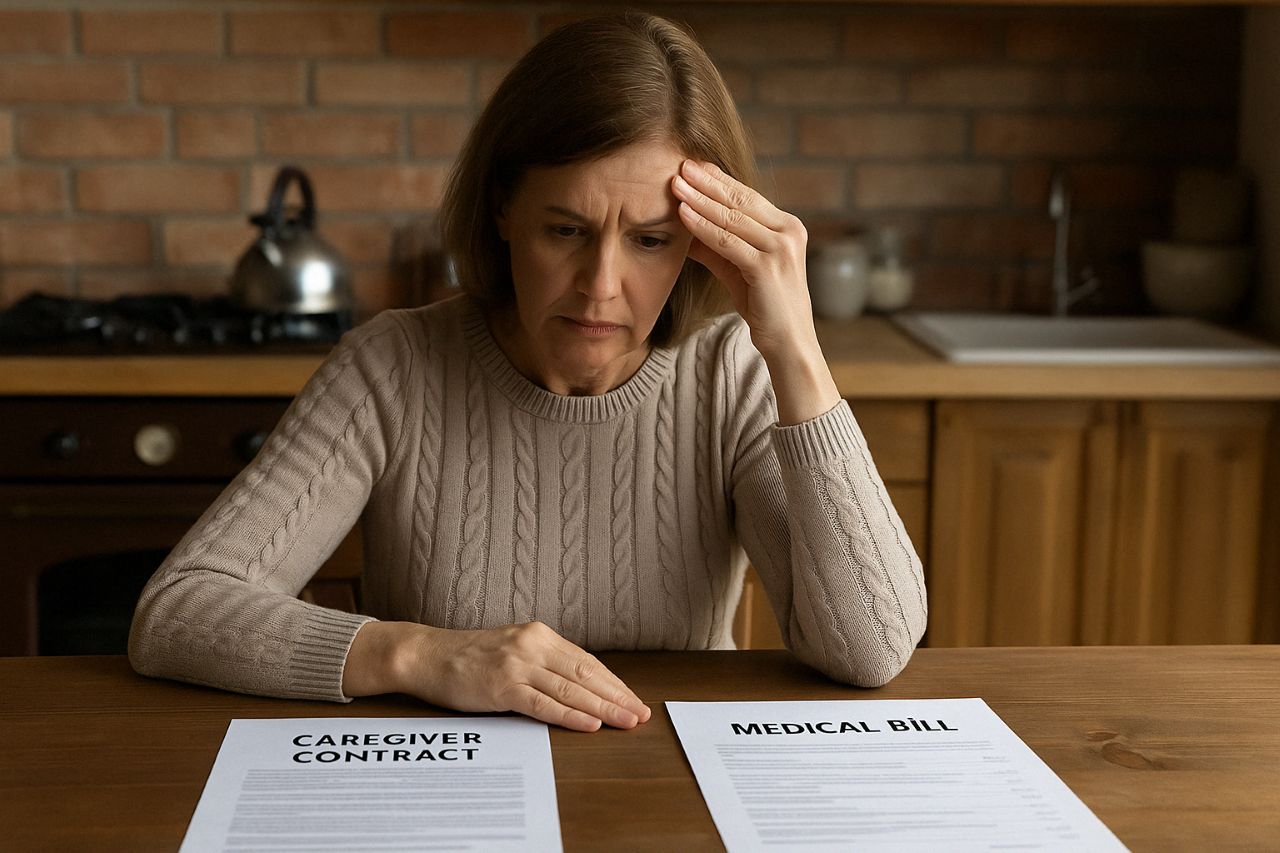

Home Health Workers Compensation Insurance is more than just a form. It is a legal and financial security network. If you hire a caregiver, you will be responsible for getting the job. Without this insurance, you could be liable for injuries, medical costs and even complaints.

Many homeowners accept standard insurance that covers everything, but that’s a costly mistake. If an accident occurs and if that happens, a proper cover will protect both you and your worker. If you understand the obligation, you can save money before and after the important set-off.

Table of Contents

What Is Home Health Workers Compensation Insurance?

Home Health Workers Compensation Insurance is a special policy that protects both employers and supervisors. Provides financial support when caregivers are breached or sick while performing a task. It covers the workplace of employees, particularly in contrast to standard homeowner or liability insurance.

In many states, this cover is needed when hiring someone regularly at home. Even if it’s not legally necessary in your state, it can provide essential protection and peace of mind.

U.S. Department of Labor – Workers’ Compensation Overview

Why Home Health Workers Compensation Insurance Absolutely Matters

It’s Not Just a Formality—It’s Financial Protection

Home Health Workers Compensation Insurance is more than just a checkbox on your to-do list. This is a powerful sign that will protect you from unexpected legal and financial storms. If you hire a caregiver to help with your daily work at home, you may not know that you will be responsibly in your employer’s shoes.

When Accidents Happen, You Could Be Liable

Even if you are comfortable at home, accidents can occur. Wet floor slips, elevators are wrong, or unexpected health events occur, and suddenly her beneficial agreement turns into legal and financial burdens. Without proper insurance, you can cover an aggravated legal action for expensive medicinal bills, loss of wages, or personal injury.

Compensation Insurance Is Your Safety Net

Home Health Workers Insurance to cover medical care, wage exchange and legal costs if caregivers are infringed at work. It ensures that your employees will take care of you and at the same time protect your savings, wealth and peace of mind. It’s not just smart – it’s responsible.

A Sign of Respect and Responsibility

When you take out Home Health Workers Compensation Insurance company, you also appreciate the security and dignity of the person you care for. For those who are older parents, children with special needs, or those who are restoring operations, workers compensation insurance can help you play your role as an ethical legal employer.

Why It’s Essential for Homeowners and Employers

You’re Legally Considered an Employer

Caregiver attitudes may feel informal, but legally, employers often pay someone for care of your home. This means you are responsible for your security while you are at work – and you are legally liable if something goes wrong.

Caregiving Is Physically Risky Work

The supervisor is not just a companion, he lifts, baths, rearranges and gives him medicine. They expose these tasks to physical stress, slides, falls, and even medical tools such as needles that can cause injury. The wrong steps can lead to serious injuries.

Without Coverage, the Costs Fall on You

Many homeowners mistakenly believe that standard home insurance will take over these situations. Unfortunately, most policies exclude household employees. This means that if you violate a caregiver, you can pay your doctor’s bill and cover your lost wages or get out of the lawsuit.

Real-Life Consequences Are Severe

There are many cases of homeowners who are blind or forced through unexpected legal action to pay large amounts simply because they are not aware of liability. A single injury can snow in tens of thousands of dollars and add stress to an already emotional situation.

Who Needs Home Health Workers Compensation Insurance?

Hiring a Caregiver? You Might Be an Employer

Take them home to your home for a few hours a week and they can be classified as an employer. This means not only paying but also being responsible for safety and wells in the workplace. This applies whether you try someone full-time, part-time, or even if you try.

Independent Hires Carry More Risk

Many families hire nurses directly without going through licensed agencies. This is more affordable and flexible, but this also means taking over the employer role yourself. This includes everything from dealing with taxes in the employee compensation context to covering injuries. The agency may take out this insurance, but when they hire them personally, they are with them.

Short-Term and Part-Time Still Count

Don’t make mistakes because you think that limited time means limited liability. Even if your caregiver comes in one week to help with food and medication, any injuries that occur during this period are legal and financial issues for you. The injury does not wait for a full-time contract. It can be held anytime.

Peace of Mind Starts with Preparation

Whether you have the help of an elderly parent, a relaxed lover or a child with special needs, accidents are only necessary to cause serious financial and legal headaches. Home Health Worker Compensation Insurance is a way to remain protected no matter how small the role is.

National Academy for State Health Policy – State Requirements

What Does It Cover?

Home Health Workers Compensation Insurance should provide comprehensive protection for both caregivers and homeowners. Here’s a detailed explanation of what is usually included in this important guideline:

Medical Expenses from On-the-Job Injuries

Home Health Workers Compensation Insurance covers your doctor’s bill if your caregiver slips into a damp floor, loads your back while lifting, or covers the needle base most while administering medication. This includes visiting a doctor, staying at a hospital, medication, and surgeries required.

Lost Wages During Recovery

If caregivers are unable to violate the entire workplace due to injuries, Home Health Workers Compensation Insurance can help replace lost income during the recovery period. This ensures you will be financially supported in healing and that you are no longer leaving your bill.

Rehabilitation or Therapy Costs

Some injuries require ongoing physical therapy, rehabilitation programs, or advice. Home Health Workers Compensation Insurance can help meet these expanded care needs and support nurses in a complete and safe return to their job.

Death Benefits in Tragic Cases

In rare but heartbreaking cases, Home Health Workers Compensation Insurance for the family of nursing staff can provide the benefits of death and death when workplace injuries result in death. It’s a difficult topic, but reporting will ensure that your relatives receive the financial support you have gained.

Legal Fees If the Worker Sues

If a dispute arises and the caregiver files a lawsuit in connection with an injury, the directive can also help cover legal defense costs. This prevents unexpected legal costs from derailing your financial stability.

Protection for Both Parties

When you take away Home Health Workers Compensation Insurance company, you don’t just fulfill your legal obligations. It also brings a safe and secure agreement to all involved. It’s about equity, responsibility and protecting your budget against life-changing financial impacts.

How to Get Home Health Workers Compensation Insurance

Start with Your Current Insurance Provider

Many large insurers offer coverage insurance to domestic officers as an addition to independent insurance or existing homeowner insurance. If you already have policies for the homeowner, the first step is to contact your provider and ask if this type of cover is available. In some cases, bundled with current guidelines can provide discounts and better terms.

Work with a Licensed Insurance Agent

As laws and requirements vary from state to state, it is important to consult with an authorized insurance agent who understands both local regulations and certain types of nursing work. You can help you assess your risk, determine your approval and find policies that meet both your legal obligations and your personal needs.

Understand What Influences the Cost

Understand what costs affect you Home Health Workers Compensation Insurance premiums typically range from $250 to $1,000 per year. Several factors affect cost:

- Location: Different states have different legal requirements and risk levels. Task: Physically demanding tasks such as patient cancellations can increase risk profiles and costs.

- Job Duties: Physically demanding tasks such as patient cancellations can increase risk profiles and costs.

- Hours Worked: The longer the caregiver works, the higher the chances of injuries that could increase premiums.

Weigh the Cost Against the Risk

Costs vary, but this is generally a moderate investment compared to the financial burden of workplace injuries. Without coverage, a single accident could result in thousands or tens of thousands of dollars of medicinal bills, loss of wages, and legal costs. You receive valuable security for hundreds of dollars a year.

Tips for Choosing the Right Policy

Choosing the right insurance for your Home Health Workers Insurance is not just about the cheapest premiums to ensure you are properly protected. Here are some important considerations to keep in mind when checking options:

Know What’s Included in the Coverage

Not all policies are the same. Ask your insurance company to disassemble what is accurately covered. Standard policies usually include medical costs, wage losses and legal defense, but also provide additional support, such as rehabilitation coverage and death benefits. Make sure the core creature is covered without hidden gaps.

Confirm Coverage for Part-Time or Temporary Workers

If your caregiver only works a few hours a week, don’t assume it’s automatically covered. Some policies exclude part-time, seasonal, or contract workers unless explicitly included. Think ahead to your supervisor’s schedule and obligations to ensure that the guidelines accurately reflect your situation.

Check State-Specific Requirements

Home Health Workers Compensation Insurance may vary significantly depending on your condition. Some states can prescribe covers immediately after hiring a few people for a certain hour, while others may not need them, but they can be recommended urgently. Authorized local agents help to control these regulations and avoid non-violations.

Ask About Exemptions and Exclusions

Each policy has several exclusions that do not apply to cover. This includes injuries caused by unauthorized activities, cases from property, or supervisors who are medical professionals licensed under separate employer agreements. Make clear what is not covered in order to avoid any unpleasant surprises later.

Understand Claim Processing Time

In the case of an injury, time is important. Ask the provider how quickly he will process his claim. Do you offer online registration? Are there any dedicated representatives? Fast and reliable claims can make a huge difference in stressful moments.

Review the Policy Carefully Before Signing

Insurance documents can be tough, but do not skip small prints. Read the complete policy and ask your agent to guide you through the terminology and clauses that are confusing. If something doesn’t make sense – ask. It is your job to explain what you sign and understand your rights.

Potential Risks of Not Having It

Employment insurance coverage for Home Health Workers Compensation Insurance appears to be harmless until an accident occurs. Without proper coverage, they far outweigh many serious financial and legal consequences. Here you risk:

Out-of-Pocket Medical and Legal Expenses

If your caregiver is injured at work and you are not covered by insurance, you can be personally liable for your treatment, physical therapy, and loss of wages. You will also cover legal costs, court costs and potential settlements from your own pocket if the violation leads to legal action.

State-Imposed Fines and Penalties

In many states, taking away Home Health Workers Compensation Insurance for domestic workers is not an option. Not violating these requirements could lead to high fines, legal estimates, or penalties that only contribute to your financial burden. Some states even classify non-violations as criminal offences.

Exposure to Lawsuits

Even if your caregiver is someone you have trusted for many years, an injury can cause legal action, especially if the insurance company is not available to cover your costs. Litigation can lead to financial decisions that put your assets, savings and even your home at risk.

Long-Term Financial Strain

The cost of the injury does not end with the first hospital visit. Continuous care, income, and legal battles can take months or years. Without insurance, these long-term costs can destroy your finances and destroy your budget stability.

Trust Isn’t a Substitute for Protection

It’s easy to assume that trust and strong relationships protect you, but the legal system doesn’t work with personal ties. Even the most loyal and well-known caregivers are advised to file or complain if the injury leads to lost income or medical difficulties. In such cases, it is not about betrayal, it is about survival.

Better Safe Than Sorry

Ultimately, Home Health Workers Compensation Insurance for health care systems is not a delusion, but a preparation. It ensures that you not only want the best but also protect yourself and those who are important to you.

Conclusion – Home Health Workers Compensation Insurance

Home health workers compensation insurance is more than just a legal custody box. It is an important investment in protection and security. By covering people who care for their loved ones, they also protect their homes, their finances, and their future.

Don’t wait for the accident to force your hand. If you know you’ve done the right thing for everyone involved, you can insurance yourself and take a break easily.

Read our article: Gap Insurance for Homes: Smart Safety Net or Costly Mistake?

Frequently Asked Questions (FAQs)

What is home health workers compensation insurance?

Home health workers compensation insurance is a type of policy that provides coverage for medical expenses, lost wages, and legal costs if a caregiver is injured while working in your home.

Do I legally need to provide workers compensation for home caregivers?

It depends on your state. Many U.S. states require employers—including private individuals hiring in-home caregivers—to carry this insurance. Always check your local laws to stay compliant.

What happens if I don’t have this insurance and a caregiver gets hurt?

Without coverage, you may be held personally responsible for the caregiver’s medical bills, lost income, and any legal claims. This can lead to serious financial consequences.

Does my homeowners insurance cover home health worker injuries?

Typically, no. Most standard homeowners’ policies do not cover workplace injuries related to in-home employees. You need a separate workers compensation policy.

How much does home health workers compensation insurance cost?

Costs vary based on location, hours worked, and job duties. On average, it ranges from $250 to $1,000 per year. Your insurance agent can provide a custom quote.

Can I get this insurance as an add-on to another policy?

Yes, some insurers allow you to add it as a rider to your existing homeowners insurance. Others may offer it as a standalone product depending on your needs.

What does this insurance typically cover?

It usually covers job-related medical expenses, lost wages, rehabilitation costs, legal defense, and death benefits if applicable.

One Comment